What Is Risk Profiling? Part 2: Let’s Stop Debating Definitions

In my previous article “What Is Risk Profiling – Part 1”, I showed how you can’t talk about, without understanding risk. And that the definition of risk has changed over the centuries due to academic research and human experience.

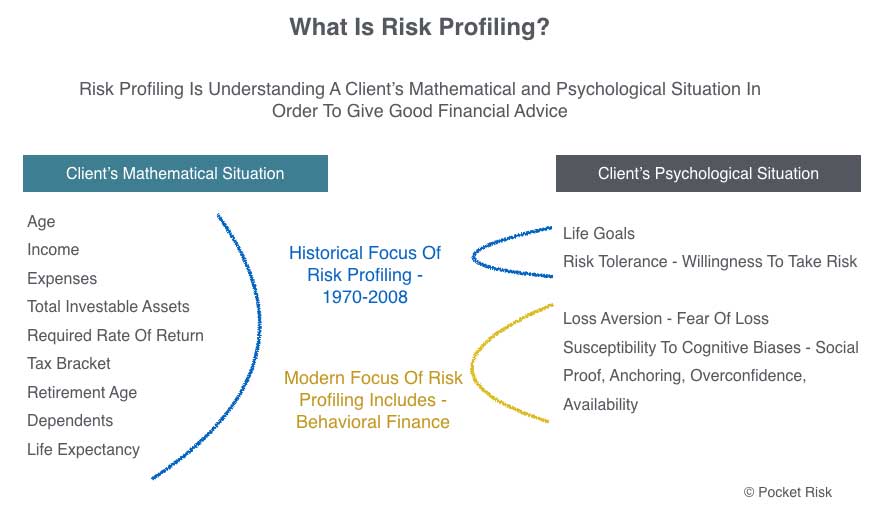

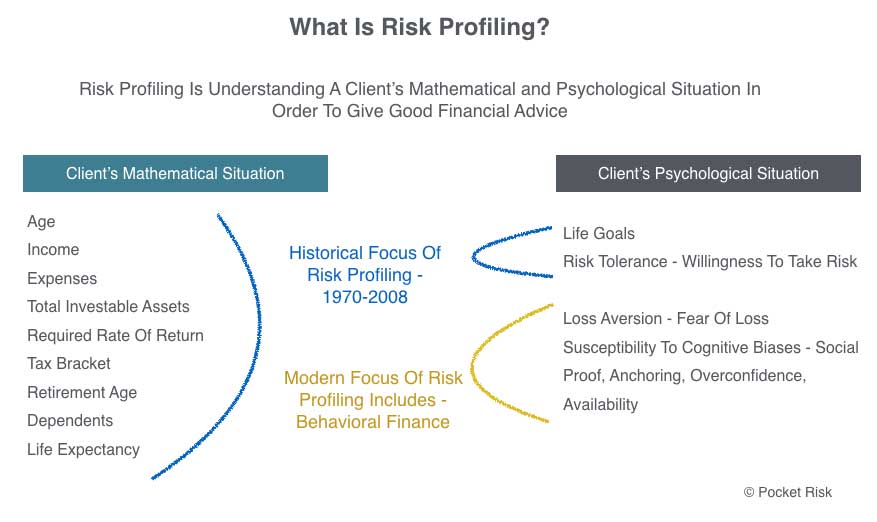

The modern consensus is that risk is a mathematical and psychological construct.

This consensus is built on over 64 years of research. It starts with the mathematical Harry Markowitz and his followers who gave us Modern Portfolio Theory and the Capital Asset Pricing Model. Most recently Friesen and Sapp have added to the psychological by publishing mutual fund data showing that “investor underperformance due to poor timing” is consistent with “return-chasing behavior”. And return-chasing behavior is primarily driven by psychological biases and a lack of financial education.

So for financial advisors, risk profiling is the process of understanding your clients’ mathematical and psychological situation in order to give good advice. Take a look at the diagram below.

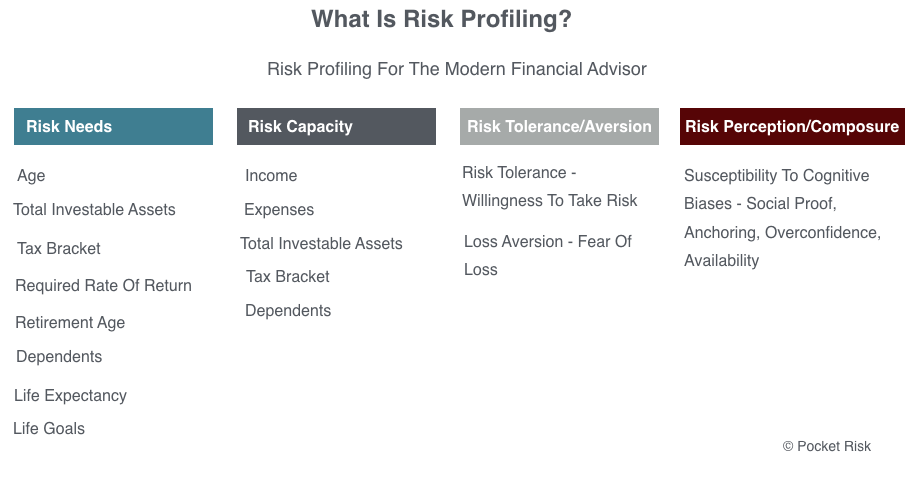

The mathematical and psychological situation of the client has been further broken down in order to translate into how financial advisors do their work. See diagram below.

According to the Ontario Securities Commission who recently undertook a study into risk profile questionnaires, the terms are defined as follows.

“Risk Tolerance: The willingness of the client to take on risk. It can be defined through their attitude towards risk and is often described as a high/low risk tolerance.” Risk Tolerance is also regarded as the opposite of loss aversion. This is backed up by research from Rozkowski, Grable, Kahneman and Tversky.

“Risk Capacity: The financial ability of a client to endure any potential financial loss. Does the client have the financial ability and can they afford to take on the risk?” This is backed up by research from Hanna, Chen, Waller and Finke.

“Risk Need: Refers to the amount of risk that should be expected in order for a client to meet specific financial goals. Larger goals may require higher returns

on investment that comes at the cost of higher risk.” This is backed up Markowitz and his followers.

“Risk Perception: A judgment that the client feels towards the severity of risk in association with the broader economic environment. This perception can be heavily influenced by the media and/or through lack of understanding of the risks. The influence of ‘risk perception’ and ambiguity aversion may be reduced by greater financial literacy, education or experience.” This is backed up by research from Friesen and Sapp.

Risk Composure: This is the likelihood that in a perceived crisis the client will behave fundamentally different to their rational self and may take action that could crystalize losses. It can be measured based on a client’s past decisions.

Risk Profile: The aggregate of all of these factors to arrive at an overall determination of a ‘sweet spot’ for a client, such that it maximizes their ability to achieve their goals but is consistent with the level of risk they are willing and can afford to take.

At Pocket Risk we agree with these definitions and the academic literature supports it.

These definitions are the culmination of decades of experiments by academics, the practical experience of advisors and increasingly the support of regulators in Canada, the UK, Australia, and India.

In order for advisors to best help their clients, they need clear definitions from regulators and the academic community. Now we have them, it’s time to build tools and practices that allow advisors to better serve their clients.

If you have any thoughts on this article, I’d love to hear them.