Is An All Cash Emergency Fund Stupid? Academics Say Yes!

September’s Journal of Financial Planning has a controversial article about emergency cash funds. Titled “Is an All Cash Emergency Fund Strategy Appropriate for All Investors?” the paper argues that a 6-month cash emergency fund comes with an “exorbitant opportunity cost” resulting in lower levels of wealth at retirement.

It’s become a sort of dictum that you should save at least 3-6 months of monthly expenses in case of emergencies. It’s the kind of advice people instinctively agree with and follow. The authors tear down this cornerstone of financial prudence and provide an impressive argument for a change in thinking.

First Things First

The authors begin their argument by invoking utility theory, which simply states investors should seek to maximize returns while minimizing volatility. Too often investors use “mental accounting” and see their wealth in buckets when they should be focused on the total portfolio. If for example they complete a risk tolerance quiz and they are shown to have a high-risk tolerance then they should apply a similar level of risk to their emergency fund.

The authors do add some important caveats. A more aggressive emergency fund should only apply to people in the “accumulation phase” of wealth building rather than those in retirement.

Secondly, it should apply to “more affluent” clients of financial advisors rather than the average Joe. I accept the first caveat but I feel the second is a little strict. Their analysis and insight can apply to people further down the income scale.

Before jumping into the reasons why an all cash emergency fund might be sub-optimal it’s necessary to state its purpose. The authors see emergency funds as having two main goals. Protect against “income shocks” (unemployment) and savings for future consumption. It is with this definition that they question what has become commonplace financial planning.

1. Insurance – The authors point to the myriad of insurance products that can protect people from income shocks. We have income protection insurance, incapacity insurance, mortgage protection insurance and many others that would soften the blow of any unemployment period. The risk of loosing a job and being unable to survive is slim given the range of products that exist.

2. Diversification – For those who want to invest their emergency fund in more volatile assets they can diversify some of their risk and see greatly improved returns. People tend to invest emergency funds in cash because it’s safe however, that does not mean investing in stocks for example is unsafe. The risk can be reduced.

3. Human Capital – The authors suggest that investors neglect to evaluate their human capital when making investment decisions. For example a college professor is likely to have a high degree of job security and could probably afford to take more risk with their emergency fund than a stockbroker. Certain jobs are safer and certain people are highly employable. If you fit into one of these categories then a more aggressive emergency fund could be appropriate to maximize utility.

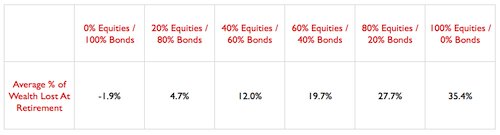

4. MAIN ARGUMENT – Opportunity Cost – To conclude their argument the authors created a model to calculate how much wealth a person would loose by not investing their emergency funds into stocks and bonds. They took an example of someone working from age 25 to 65 assuming average levels of unemployment. Stock and bond data ran from 1926 to 2011.

The results were staggering. If an individual invested their 6-month emergency fund in a 60/40 portfolio instead of cash they could expect to have up to 20% extra in retirement savings. This clearly calls into question the requirement for a 6-month emergency cash fund given the assumption you want to maximize returns. The question investors need to ask themselves is whether the peace of mind of having cash in the bank, is worth loosing up to 20% of potential retirement savings.

Concluding Thoughts

The authors make a compelling argument against the 6-month emergency cash fund. However, beyond a client’s risk tolerance and the possible use of a risk tolerance questionnaire they didn’t look at other risks. Notably, counter party risk (getting access to your insurance or investment from a provider).

Utility theory might tell us what is optimal but it fails to account for the behavioral psychology aspect of the human mind when it comes to investing. Regardless, the authors have made a compelling argument and if they can’t get investors to entirely drop the 6-month emergency cash fund I am sure more than a few would consider switching to three months.